Financial Control using a Simple Spreadsheet

I know how annoying it can be to update a Financial Control Spreadsheet adding each expense, to use different apps or any other financial tools that make you lose time without giving a real control of our financial situation. After trying many alternatives to handle with that I build my own way to deal with my financial control without be a painful and timing cost.

I’ve been done some work on this financial-spreadsheet, in order to create a tool and a methodology to financial empower ourselves. I believe is one of the most important pillars in our modern society otherwise you will always be a slave of your money but it’s your money which needs to work for you to build your wealth. It’s just a simple spreadsheet and a few steps to follow but it will help you to take control of your financial life. (few free to copy and edit as your needs)

Firstly, forget about daily updates and lots of inputs.

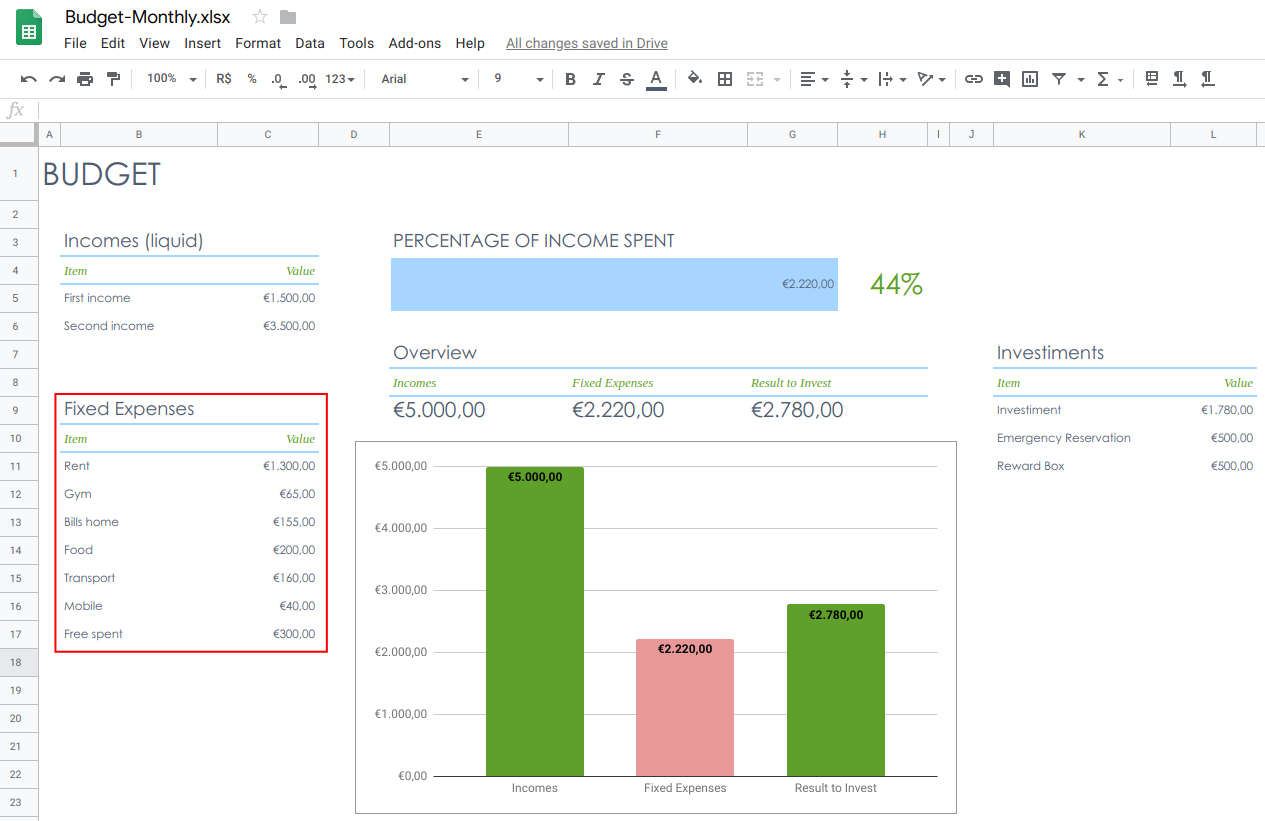

Secondly, set up your incomes as shown in the red rectangle below. Incomes (liquid).

Thirdly, set up your minimum expenses as shown in the red rectangle below. Fixed Expenses. It means the bills that you can’t cut off. Each person have your own necessities so this part is private but in the end, you need to have a positive outcome otherwise you need to think in create extra incomes and cut expenses.

You can’t live one step above of your actual financial situation the ideal world is live one step down.

*Tip: add a bill called Free spent it’s from here that you get money for a coffee or lunch.*

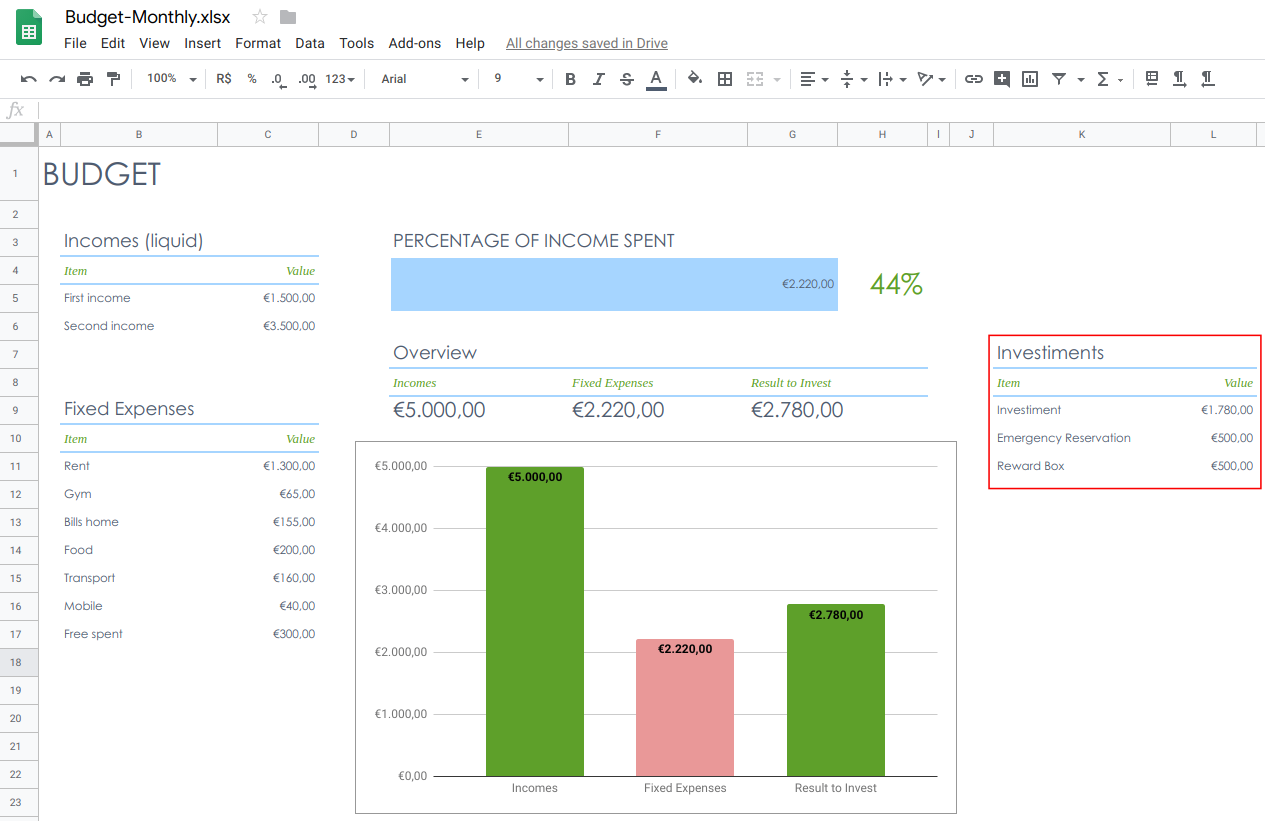

Finally, add the money destined to save/invest as a bill and this will deduce before you pay the “minimum expenses”. The investment is not optional or something that you do when remaining money at the end of the month. It is like a bill that you must to pay to yourself for your monthly effort.

I personally slipt my investment within three “categories”: 1- General Investment: Stocks, ETF, Business, Gold, Coins and Education. In the nutshell is money that you will invest in the mid-long term. 2- Emergency Reservation: 4–6 months of your Fixed Expenses.The money needs to stay in a liquid place (saves account/liquid applications) for easy access in case of an emergency that can happen eventually. The main goal of this money is liquidity, not high interests. The Emergency Reservation won’t let you rich; It's a duty of your incomes and *general investments. *The most important is: this money is only for emergency (lose your job or health problems). After you save 4–6 months you can stop save the Emergency Reservation and start to focus only intoGeneral Investiments . 3- Reward Box: you must have 10–30% of your investment destined to enjoy as you wish. It’s your Reward Box which you will do whatever you want, as a trip, buy expense things... The main idea with that box is to fund the biggest things that you find important in your life.

In the nutshell, it should be a great picture of your incomes and outcomes (passive/active). Following this method, you will have a better overview of your finances and you just need to check and update once a month.

Vinicius S. https://vstevam.com